For most of recorded history, India’s population story was defined by growth, relentless, extraordinary, and seemingly without a ceiling. At independence in 1947, the country had a population of roughly 340 million. By 2023, it had surpassed China to become the world’s most populous nation, with a population of 1.45 billion.

That trajectory, spanning less than eight decades, represents one of the largest demographic expansions any society has ever produced. Yet the era of growth is, quietly and unmistakably, approaching its end. India’s population peak is now a matter of when, not whether, and the date most analysts, demographers, and international institutions converge on is somewhere in the early 2060s.

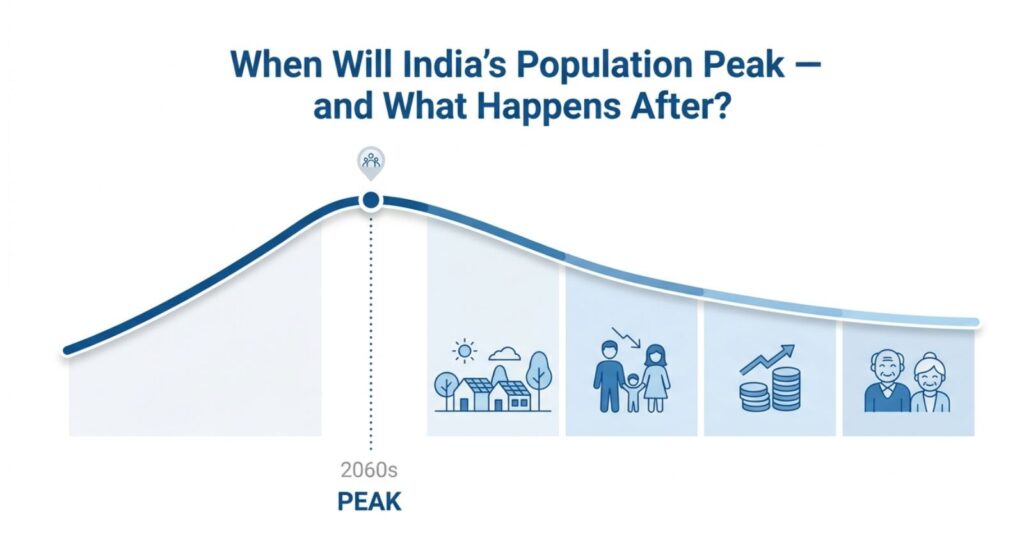

According to the United Nations World Population Prospects 2024 report, India’s population is projected to peak in the early 2060s at approximately 1.7 billion, after which it will decline by around 12 percent. Despite that decline, India is expected to remain the world’s most populous country throughout the entire century. That is a remarkable statement on its own terms: a nation contracting in absolute numbers, yet still holding more people than any other country on earth. The gap between India and the rest of the world’s population rankings will be measured in hundreds of millions even after the peak is passed.

What makes this moment uniquely consequential is not the peak itself but what follows it. A post-peak India will look structurally different from the country it is today. The median age will rise, the youth bulge that powered decades of economic optimism will flatten, and the dependency burden will shift from children to the elderly. Fertility rates that once seemed immovably high have fallen faster than most models predicted. The forces behind India’s coming demographic inflection point are already well in motion, and understanding them is essential to understanding what India’s next fifty years will actually look like.

Why India’s Fertility Rate Fell Faster Than Expected

The standard explanation for India’s fertility decline points to education, urbanization, and access to family planning. Those factors are real. But the speed and depth of the decline have genuinely surprised demographers. Data from National Family Health Surveys shows that India’s Total Fertility Rate (TFR) dropped from 3.39 in 1990–92 to 2.0 in 2019–21, crossing below the replacement threshold of 2.1. That is a halving of the fertility rate in under three decades, a pace that compressed demographic transitions that took over a century in many European nations.

The structural drivers are layered. Female literacy climbed from approximately 39 percent in 1991 to nearly 70 percent in 2021. Women with 12 or more years of schooling have a TFR of 1.7, compared to 2.8 for women with no formal education, according to NFHS-5 data. Urbanization accelerated that shift further. Raising a family in a major Indian city carries costs that simply did not exist in the rural household economy of earlier generations. Smaller living spaces, higher education expectations, dual-income necessity, and delayed marriage patterns all converge to suppress birth rates organically.

The rural-urban divide in fertility is still measurable, but it is narrowing. TFR in rural India has now reached replacement levels as of 2023, having once been substantially higher than in urban areas. Urban India reached replacement fertility as early as 2004. That convergence signals that the fertility transition is no longer confined to India’s more prosperous, educated southern and western states. It has spread.

The North-South Fertility Divide

India’s fertility story is not uniform, and that non-uniformity matters enormously for projections about when and where the peak actually arrives. All eight southern and four western states now report TFRs below 2.0, indicating early population stabilization and the beginning of ageing pressures. Tamil Nadu’s fertility rate is already comparable to that of Norway. Andhra Pradesh, at 1.5, sits near EU-level fertility. The northeastern state of Sikkim has seen its TFR plunge to 1.1, prompting the state government to introduce financial incentives for employees with more than one child, along with free childcare and paternity leave.

The north is a different story. States like Bihar, Uttar Pradesh, and Jharkhand remain above replacement level. Bihar, with a poverty rate of around 32 percent, records a TFR of 3.0, the highest in the country. This is where population growth momentum will be concentrated for the next two to three decades. These states are also younger, less economically developed, and have weaker healthcare and education infrastructure, a combination that historically sustains higher fertility for longer.

The demographic consequence of this internal divergence is significant. Southern states will begin experiencing the economic and social pressures of ageing populations, while northern states are still producing a surplus of young workers. That creates a potential internal labor migration dynamic that could ease, though not eliminate, the transition pressures each region faces individually.

What “Demographic Momentum” Means for the Peak Date

Even after a country’s TFR falls below replacement level, the population continues to grow for decades. This is demographic momentum, the product of an age structure still thick with young adults in their childbearing years. India is living this phenomenon precisely right now. Population growth in India will continue, concentrated mostly in the northern states, on the basis of demographic momentum resulting from a large number of young adults still in childbearing years.

At the turn of the millennium, India was adding nearly 20 million people annually to its population. By 2024, that figure had declined to under 13 million per year, and India is expected to stop adding net new people entirely around 2060, after which absolute population decline will begin. The slowing is visible, but the inertia of a 1.45-billion-person population means the machine does not stop overnight.

The youth population aged 15 to 24 years will reach its maximum share of the total population by 2025, after which India will progressively move toward ageing. The working-age population in the 25 to 64 years cohort will continue to increase until 2040, after which it is projected to decline alongside a simultaneous increase in the proportion of the elderly. That 2040 plateau of the working-age population is arguably the more consequential inflection point for economic planning than the population peak itself.

Population Projection Scenarios: The Range of Outcomes

Not every model agrees on a single number. The UN’s World Population Prospects 2024 report represents the most widely cited baseline, but alternative scenarios carry meaningfully different implications.

| Scenario | Peak Population | Peak Year | TFR Assumption | Population by 2100 |

|---|---|---|---|---|

| UN Medium (WPP 2024) | 1.70 billion | Early 2060s | Declines to ~1.8 by 2035 | ~1.5 billion |

| UN Low Variant | ~1.5 billion | ~2040 | Falls rapidly to ~1.3 | ~900 million |

| IASP/UNFPA 2025 | 1.8–1.9 billion | ~2080 | Slower decline assumed | Higher |

| IHME/GBD Projection | Steep decline post-peak | Post-2060 | TFR to 1.04 by 2100 | Below 1.0 billion |

| Education-Adjusted Model | 1.70–1.78 billion | 2060–2075 | TFR ~1.7 by 2040 | ~1.1–1.3 billion |

The most probable scenario as of late 2025 is a population peak of 1.70 to 1.78 billion between 2060 and 2075, driven by faster-than-anticipated fertility decline visible in the newest UDISE+ education data and UNFPA models. Several uncertainties remain, including regional fertility variation, especially in Uttar Pradesh and Bihar, potential policy changes, and climate or migration shifts that could alter the peak by up to 0.05 billion in either direction.

The Demographic Dividend: An Expiring Window

India has long been positioned as the beneficiary of a historic demographic dividend, the economic acceleration that occurs when a large working-age cohort supports a relatively small number of dependents. That window is real, but it is not permanent. With 68 percent of India’s population in the working-age group of 15 to 64 years, the country still holds a significant demographic dividend. However, this window is not infinite.

By 2030, one out of every five working-age people in the world is projected to be Indian. To sustain that potential, India will need to add approximately 7.85 million jobs every year until 2030. That is the employment imperative behind the demographic dividend, and it is one India is still grappling with. Over 30 percent of Indians aged 15 to 30 years are neither in employment nor in education and training, more than double the OECD average and nearly three times that of China.

India’s economy can no longer grow on the back of its demographic dividend alone. Fertility rates have fallen below replacement levels across states and income groups, the working-age population will plateau by the early 2040s, and the old-age dependency ratio is already rising. The country faces what economists call the productivity imperative: when headcount can no longer drive growth, output per worker must fill the gap. That requires investment in skills, technology, capital deepening, and institutional reform, precisely the areas where India’s policy record has been uneven.

What Happens After the Peak: The Ageing Transition

The post-peak era does not arrive with a single dramatic announcement. It accumulates. The first signal is visible in school enrollment data: fewer children entering the education system. The second is a labor market that stops expanding on its own. The third, and most consequential over the long term, is the rapid ageing of the population.

By 2050, older adults aged 60 and above are expected to make up nearly 20 percent of India’s population, roughly 320 million people. Between 2022 and 2050, the population aged 80 and above will grow by 279 percent. To put that in context, 320 million elderly Indians would constitute a population larger than the entire United States today.

India’s old-age dependency ratio, estimated at 16 per 100 working-age individuals in 2021, is projected to rise to 30 by 2050. That means for every three working-age individuals, one person aged 60 or above will exist as a dependent. The fiscal, healthcare, and caregiving implications of that shift are substantial. Seniors are significantly more expensive to support than children: they require pensions, geriatric healthcare, long-term care facilities, and social protection systems that India has not yet built at the necessary scale.

The Healthcare System Under Pressure

Approximately 80 percent of older adults in India currently suffer from at least one chronic condition, including diabetes, hypertension, or osteoarthritis. Mental health issues affect around 15 percent of the elderly, but are frequently underreported due to social stigma. An ageing population with high chronic disease burden represents a structural challenge for a healthcare system that has historically been organized around younger populations and acute care.

Non-communicable diseases are projected to cost India an estimated 4.3 trillion dollars in productivity losses and healthcare costs between 2012 and 2030. As the elderly share of the population grows, those costs will multiply further. India’s public health expenditure has historically hovered around 1 percent of GDP, a level that most public health analysts consider deeply inadequate relative to the system demands that are coming.

Pension and Financial Security Gaps

India’s elderly population currently stands at 153 million aged 60 and above and is expected to reach 347 million by 2050. Within that population, 40 percent are in the poorest wealth quintile, and about one-fifth have no income at all. A social protection system built for a young population, where family structures traditionally absorbed elder care, will face structural stress as urbanization and nuclear family formation reduce informal support networks.

In the absence of a robust and universal social security system, with low coverage of old-age pensions, a large share of employment in the informal sector, early retirement from formal employment, and increasing health expenditure, elderly households in India are economically vulnerable and prone to financial shocks. These vulnerabilities are not hypothetical; they are already documented in current elderly populations, and they will scale with the demographic transition.

The Silver Economy: An Underappreciated Opportunity

A rapidly ageing population is not only a liability. It creates an entirely new economic demand frontier. The silver economy, the sum of economic activity serving the needs of people aged 50 and older, opens a vast space for India’s startups and disruptors to provide accessible, cost-effective, and inclusive solutions catering to the specific needs of older persons.

Senior wellness, eldercare facilities, age-appropriate housing, health tech, telemedicine, insurance products for the elderly, and retirement financial services are all industries at nascent stages in India today. The scale of need that will exist by 2050 will create markets comparable in size to entire sectors of today’s economy. Technology can be an important differentiator in the delivery of these services, with health tech, telemedicine, and AI-driven diagnostics ensuring medical services at scale. Countries like Japan and South Korea have spent decades building institutional frameworks for ageing societies. India has perhaps two decades to build its own.

India’s Population After 2060: A Country Still Dominant, but Changed

The post-peak population trajectory, even under the UN’s medium scenario, does not produce a depleted India. By the end of the century, India is projected to be around 1.5 billion, still the largest country in the world by a large margin. By comparison, China’s population is expected to fall from a current level of 1.4 billion to just 600 million by 2100, a decline of over 50 percent. India’s post-peak contraction, measured in relative terms, is far gentler than what China faces.

What changes is the internal character of that population: older, more urban, with a median age rising steadily, and with regional demographic asymmetries that will shape political representation, labor allocation, and fiscal federalism in ways that India’s current institutional framework is not yet designed to handle. States that aged earliest, largely in the south, will increasingly rely on labor migration from northern Indian states. That internal redistribution of human capital is one of the most underappreciated dynamics in India’s coming demographic story.

The long arc of India’s population history bends, ultimately, toward stabilization. The country will not shrink into irrelevance; its sheer size guarantees global weight for another century at minimum. But the age structure that underlies that population will demand a fundamentally different model of governance, investment, and social organization than the one that served the growth era. The decisions India makes between now and 2040, on pensions, healthcare infrastructure, elder care, female workforce participation, and skills, will determine whether the post-peak decades are managed with resilience or arrive unprepared.

FAQ

1. When exactly will India’s population peak?

India’s population is projected to peak in the early 2060s at approximately 1.7 billion, according to the UN World Population Prospects 2024 report. Some alternative models, incorporating newer fertility data, suggest a peak between 2060 and 2075, with the population stabilizing at between 1.70 and 1.78 billion.

2. Will India always remain the world’s most populous country?

India is expected to remain the world’s most populous country throughout the entire 21st century, even after its population begins to decline following the peak. By 2100, India’s population of approximately 1.5 billion will still exceed that of any other nation by a substantial margin.

3. What is India’s current Total Fertility Rate?

India’s TFR dropped to 2.0 in 2019–21, falling below the replacement level of 2.1 for the first time. State-level data shows TFR ranging from 1.4 in Delhi and West Bengal to 3.0 in Bihar, reflecting wide regional variation in demographic transition.

4. Which Indian states are growing fastest in population?

Only five Indian states, Bihar, Meghalaya, Uttar Pradesh, Jharkhand, and Manipur, remain above the replacement-level fertility of 2.1. These states, concentrated in central and northern India, are driving the remaining national population growth through demographic momentum from large young populations.

5. What does “demographic dividend” mean for India, and how long does it last?

The demographic dividend refers to the economic acceleration possible when a large share of the population is of working age, and the dependency ratio is low. India’s working-age population in the 25 to 64 age group will continue to increase until 2040, after which it is projected to decline alongside a rising proportion of elderly citizens. The dividend window is therefore roughly the next fifteen years.

6. How will India’s ageing population affect the economy?

India’s old-age dependency ratio, currently at 16 per 100 working-age individuals, is projected to rise sharply to 30 by 2050, meaning one elderly dependent for every three working-age adults. This shift will increase fiscal burdens for healthcare, pensions, and social protection while reducing the workforce share that has traditionally driven economic growth.

7. How does India’s demographic trajectory compare to China’s?

India’s population is projected to grow until around 2060, peaking at roughly 1.7 billion before declining gradually to about 1.5 billion by 2100. China, by contrast, has already begun to shrink, with its population expected to fall from 1.4 billion to just 600 million by 2100, a decline of over 50 percent.

8. What happens to India’s youth population after the peak?

The youth population aged 15 to 24 years will reach its maximum share of India’s total population by 2025, after which the country will move progressively toward ageing. By 2060, India’s aged population over 65 years will outnumber both the 0 to 4 and 5 to 14 age cohorts combined.

9. What is driving fertility decline in India so rapidly?

Multiple factors converge: rising female literacy, later marriage ages, urbanization, improved child survival rates, reducing perceived need for large families, and expanded contraceptive access. TFR in urban India reached replacement fertility as early as 2004, and rural India crossed that threshold around 2023. The transition is now essentially national, not regional.

10. How should India prepare a policy for a post-peak population?

The investments India makes in the next five years, in skills, technology, healthcare, and state capacity, will determine its economic trajectory for the next fifty years. Productivity gains take years to compound, and human capital and infrastructure take a decade to mature. Building universal pension coverage, scaling geriatric healthcare, increasing female workforce participation, and developing the silver economy are the structural priorities that demographers and economists most consistently identify.